California is more at risk of flooding than previously thought.

More than 655,000 additional properties in California currently not identified by federal mapping face a substantial risk of flooding over the next 30 years, bringing the total across the state to 1,150,800. Properties facing any risk of flooding by 2050? The total number rises to over 2.2 million.

In fact, the entire United States has a whole new picture of the significant risks we face from flooding today, and how that will increase into the future, thanks to an independent analysis by First Street Foundation based in New York. For the first time, they have disclosed flood risk data—at the individual property level—across the nation, available for free.

From their analysis, roughly 6 million more properties and property owners in the U.S. are at substantial risk of flooding, and likely had no prior idea of this threat or were underestimating their risk level.

Taking an even broader look at the number of properties facing any risk of flooding, the researchers found that means almost 24 million properties in the U.S. are in danger of flooding over the next 30 years.

For someone who gets excited reading about the latest climate risk maps, this novel research is a pretty big deal. Up until now, our collective decisions about where to buy or build a home, approve construction, or even sell insurance have not been fully informed!

Through this research, we are leveling the playing field of access to flood risk information and bringing transparent and robust climate risk considerations to the forefront for individuals, governments, and private sector actors to incorporate in their decision making.

How is this possible? Haven’t we been mapping flood risk for years?

Shortcomings of FEMA Flood Maps

The U.S. has been mapping flood hazards since 1969, spending more than $10 billion in such efforts. The Federal Emergency Management Agency (FEMA) and the National Flood Insurance Program oversee flood hazard mapping, maintaining and updating Flood Insurance Rate Maps and risk assessments.

It will come as no surprise that the FEMA flood risk maps are not perfect. To start, they are based on historical data. Sometimes 50-year old models are used to predict storm surge. For some areas of the country, FEMA hasn’t yet mapped flood risk, so the data simply does not exist.

FEMA mapping also does not take into account flooding caused by heavy rainfall, but rather focuses on the flooding caused by overflowing rivers and creeks. This is clearly problematic when California’s storms are becoming more intense with climate change, and the Bay Area, in particular, will likely continue to see more frequent “whiplash” events that swing from extremely dry to extremely wet conditions. Heavy rainfall hitting impervious surfaces in our urban environments leads to significant urban flooding and water quality problems nowhere near an overflowing river.

Most importantly, FEMA flood maps have traditionally been used by government actors in flood mitigation planning, informing decisions about zoning, land use, building standards, where to approve construction and more. They are also made to determine flood insurance rates. FEMA flood maps are not primarily geared towards informing individual understanding of personal flood risk.

Here’s in a nutshell what we are now getting with the new maps by First Street Foundation:

- Climate-adjusted maps, meaning they are taking future impacts from a changing climate into consideration. Their analysis also integrates current and future environmental considerations into the mix. This means that the number of at-risk properties in the U.S. will grow by another 11% or 1.6 million under warming atmospheric conditions. Climate change will continue to increase the population living in vulnerable, flood-prone areas.

- Broader coverage, providing information for every property in the contiguous U.S. For Californians, this translates to 2.2 times more properties identified by First Street Foundation as having flood risk compared to what FEMA has currently mapped.

- A fuller picture of a higher “flood” risk, including any type of flooding, whether from inundation from riverine overflow, rainfall, storm surge, or tidal sources.

This new data reveals that one in 10 American properties are at significant risk of flooding.

Increasing Flood Risk in the Bay Area

This research points to a much broader level of risk of flooding in the Bay Area than currently mapped by FEMA. For example, the city of San Jose has the fourth-highest number of properties at risk of flooding in the state with 56,243 properties currently at risk of flooding today. That’s 25% of its total number of properties! For Santa Rosa, while the absolute number isn’t as high—19,914 properties are at risk of flooding today—that amounts to a whopping 37% of its total number of properties currently at risk.

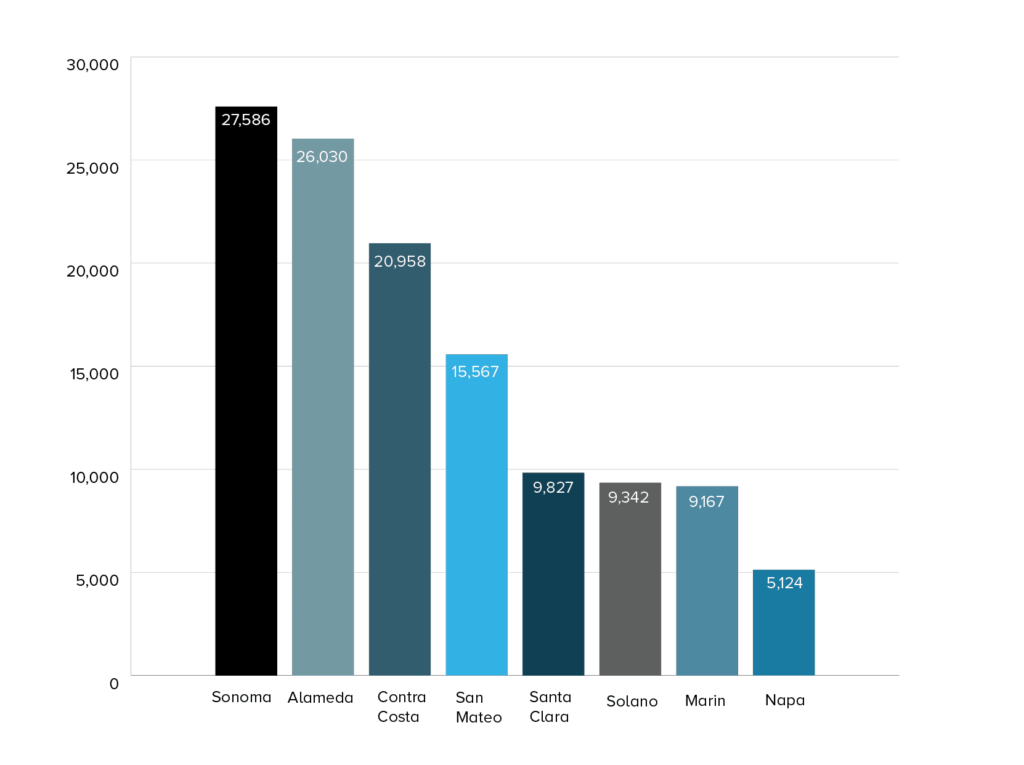

Looking by county, here are the additional number of properties at risk compared to what is mapped by FEMA.

Increase in Bay Area Properties At Risk of Flooding

- 27,586 increase in Sonoma

- 26,030 increase in Alameda

- 20,958 increase in Contra Costa

- 15,567 increase in San Mateo

- 9,827 increase in Santa Clara

- 9,342 increase in Solano

- 9,167 increase in Marin

- 5,124 increase in Napa

How should we apply these new maps?

Homeowners: A Call to Adapt

If you are a homeowner, go check out your property’s “flood factor” that First Street Foundation has made available through this new tool based on past floods, current risks, and future projections. The group is also working on integrating its new analysis into Realtor.com.

What this means is that now current homeowners, as well as prospective buyers and sellers, have more information readily available and a way to easily understand the level of flood risk associated with a given property.

This data should be a welcomed insight so that a property owner can plan proactively to address flood risk head-on with adaptation measures individuals can take, ranging from disconnecting downspouts to installing rain gardens and landscaping with native absorbent plants.

Communities & Advocates: Information to Focus Equitable and Resilient Investments

Community groups and advocates can also apply this new data to pinpoint people and areas needing additional attention—pushing for increased government investments and regional coordination, infrastructure upgrades, and adaptation measures in areas where homeowners can’t afford to fit the bill themselves. The scale of flooding risk and the rate at which we need to adapt will require collective action at a regional scale. We won’t truly build long-term resilience to flooding by taking actions property by property, or even city by city.

Things get a bit tricky when we start to consider what this heightened information and transparency of risk might do to property values. If we are not careful on how we collectively respond to this new data, we could inadvertently be furthering disinvestment in places at high flood risk, desperately needing to build resilience.

We are reminded by the major nationwide flood events, and here at home with the Bay Area’s first regional assessment of sea level rise, that communities facing significant flood risk are also facing social and environmental injustices, and the impacts of flooding exacerbate existing social and racial inequities. Marginalized communities in the Bay Area, especially low-income and communities of color, may be heavily impacted by sea level rise in the coming decades.

If, because of actual flood losses or a perceived future flood risk, properties begin to decline in value, that could further erode the tax base traditionally tapped to pay for infrastructure upgrades and other adaptation investments.

This could also impact the accessibility and availability of mortgage lending as chairman of the Mortgage Bankers Association, Michael Berman points out. He warns that if we don’t reduce and manage flood risk, “there may be a threat to the availability of the 30-year mortgage in various vulnerable and highly exposed areas.” The result, decreased homeownership and a decreased tax base for channeling investments back into communities, and the cycle continues.

We must apply this new flood-risk data with caution and better analyze the potential for this information to inadvertently perpetuate systemic racism and inequitable outcomes. To that end, First Street Foundation has created the First Street Foundation Flood Lab, where academic researchers and industry experts will continue to analyze the implications of this new flood risk data on low-income and disadvantaged communities.

Insurers: Incentivize Reducing Risks

Now is the time for the insurance industry to price climate risk accordingly. Set insurance policy premiums at higher rates as a disincentive to build or purchase homes in high flood risk areas. Charge lower financing and insurance premium rates to individual homeowners and buyers who take steps to lower their flood risk.

If we are now adding 6 million more properties under this revised assessment of flood risk, that likely means homeowners or businesses on any of these properties may not have considered the need to take out a flood insurance policy!

Here’s a chance for the insurance industry to innovate with new products. I listened to a webinar hosted by Munich Re where they spoke about things like community-based insurance. Policies can be drafted for an entire neighborhood, and provide some financial resources at that group level in addition to federal systems of risk coverage. For underserved communities where individual insurance may be too costly, this community-level option could provide heightened protection while also generating new revenue streams for the insurance industry.

Governments: Prioritize Investing in Resilience

After a flood event, the federal government issues payments as a form of climate bailout without requiring much in exchange for commitments to build back better or leave dangerous places altogether. This updated mapping could fuel a paradigm shift away from relying on and waiting for, the federal government to help after a flood event, and instead shift the focus on pre-disaster investments that build resilience.

We now have better information to help us mitigate our flood risks, seeing the broader picture of places at risk today and where to coordinate efforts and share best practices to reduce our risks. With a climate-adapted model, government actors should examine this data and prioritize adapting today ahead of the looming climate disasters and extensive flood damage likely to strike, reaping long-term benefits to communities through climate resilience investments.

Everyone: Incorporate Climate Risk Data Into Decisions

According to recent congressional testimony by FEMA’s Assistant Administer for Risk Management, Michael Grimm, in the last decade, floods alone have caused over $155 billion in property damages and they continue to account for the majority of federally declared disasters.

There is no doubt now that flooding is the most common and costly natural disaster in the United States.

First Street Foundation has sounded the alarm: as a nation, we have more places at risk of the climate impacts of flooding than previously thought, and this will increase into the future. With this research made public, homeowners, governments at all levels, the insurance industry, advocates for climate resilience, everyone now has the same information. We must all apply this in our decision-making to incentivize collective actions that lower our flood risk and create a society that is more resilient today and prepared for the flooding of tomorrow.

Photo: Kelly Sikkema via Unsplash